Because the Bitcoin market confronted turmoil surrounding the attainable chapter of Genesis Buying and selling and Digital Forex Group (DCG), chatter saved surfacing that Michael Saylor’s and MicroStrategy’s Bitcoin wager could possibly be in jeopardy if the value continues to fall.

This elephant within the room has been investigated by Will Clemente of Reflexivity Analysis and Sam Martin of Blockworks Analysis. Of their report, they study the questions of whether or not MicroStrategy has a Bitcoin liquidation worth, how excessive it’s, and the way the corporate’s debt is structured.

MicroStrategy has the biggest Bitcoin holdings amongst exchange-listed corporations, amounting to 130,000 BTC. Previously, the corporate even took out new loans to develop its Bitcoin holdings.

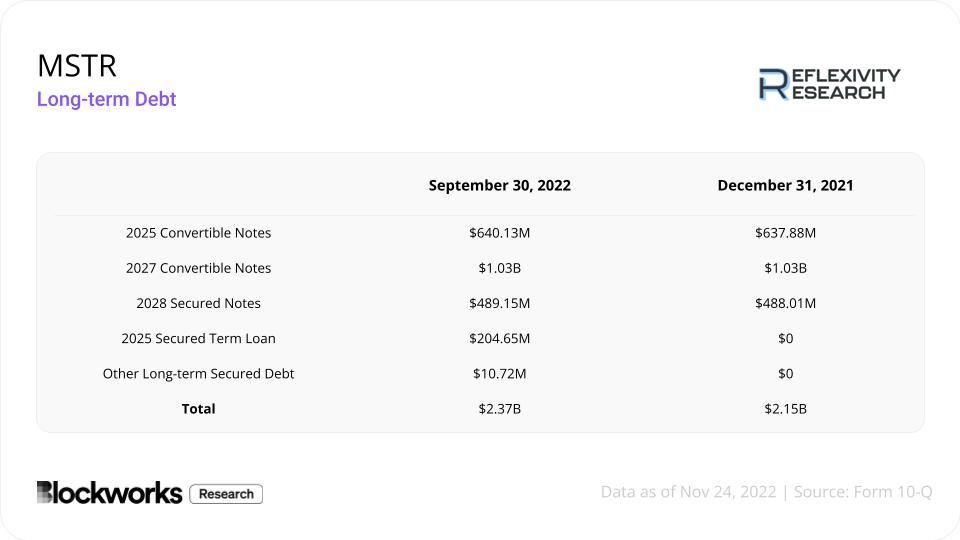

Particularly, MicroStrategy borrowed $2.37 billion to purchase its Bitcoin at a median worth of about $30,000 per BTC. The debt profile of Saylor’s firm may be discovered within the desk beneath.

Is MicroStrategy And Saylor’s Levered Bitcoin Guess At Threat?

The convertible notes incur minimal curiosity prices for MicroStrategy, in keeping with the analysis report, as a result of the notes have been issued at very favorable MSTR conversion charges.

As well as, conversion to inventory can not happen till June 15, 2025, and August 15, 2026, on the earliest, except the corporate undergoes a “elementary change.”

In line with Reflexivity Analysis, that is the case with a NASDAQ or NYSE delisting, a merger or acquisition of MicroStrategy, or a change in majority possession of the corporate.

Since Michael Saylor owns 67.7% of the voting rights, the latter situation could be very unlikely, making the convertible notes not a serious threat.

The 2028 senior secured notes, then again, are dangerous for a number of causes, in keeping with the report. They embody a excessive mounted rate of interest, tie up 11.5% of BTC holdings, and will trigger issues if the maturity date is triggered.

“Nonetheless, it poses no speedy risk to MicroStrategy,” Blockworks Analysis mentioned.

For Silvergate’s $205 million secured mortgage in 2025, with about 85,000 liquid BTC, Saylor’s liquidation worth for that mortgage is reached at a Bitcoin spot worth of $3,561. Thus, this additionally doesn’t pose a right away threat. Reflexivity Analysis states:

Whereas the aforementioned dangers to MicroStrategy and its BTC reserve are comparatively far out from changing into speedy issues, the larger fear lies within the firm’s potential to service the curiosity on its excellent debt.

MicroStrategy’s working outcomes from its software program enterprise present a big decline in profitability, and a possible recession may additional impression working outcomes.

In its newest 10-Q report, the corporate itself warns that it may undergo working losses in future durations. On the similar time, Saylor’s firm holds almost $67 million in liquid property, which is able to function a buffer over the following 6-12 months.

As well as, the corporate has about 85,000 liquid BTC on its steadiness sheet to prime up collateral ought to Bitcoin fall beneath $13.5,000 and push the loan-to-value ratio of the Silvergate mortgage above 50%.

“Nonetheless, the software program enterprise wants to select up so as to keep away from compelled BTC promoting in 2024,” Blockworks Analysis concluded. For now, nonetheless, MicroStrategy’s Bitcoin wager is nothing traders must be worrying about.

At press time, the BTC worth was rejected as soon as once more from the foremost resistance at $16.600.

Slips Further As Bears Target Deeper Support Zones")