Introduction

Based in 1989, MicroStrategy is a U.S. firm that gives enterprise intelligence, cellular software program, and cloud-based providers. Led by Michael Saylor, considered one of its three co-founders, the corporate noticed its first main success in 1992 after touchdown a $10 million contract with Mcdonald’s.

All through the Nineteen Nineties, MicroStrategy noticed its income develop by over 100% yearly because it positioned itself as a pacesetter in information analytics software program. The onset of the dot.com increase within the late Nineteen Nineties supercharged the corporate’s development and culminated in 1998 when it went public.

And whereas the corporate has been a staple of the worldwide enterprise surroundings for many years, it wasn’t till it acquired its first Bitcoins in August 2020 that it got here below the radar of the crypto trade.

Saylor made information by making MicroStrategy considered one of a handful of public firms to carry BTC as a part of its treasury reserve coverage. On the time, MicroStrategy stated that its $250 million funding in BTC would supply an inexpensive hedge towards inflation and allow it to earn a excessive return sooner or later.

Since August 2020, the corporate has periodically been buying giant portions of Bitcoin, affecting each the value of its inventory and BTC.

On the time of MicroStrategy’s first Bitcoin buy, BTC was buying and selling at round $11,700, whereas MSTR was buying and selling at roughly $144. At press time, Bitcoin’s value hovers round $22,300 whereas MSTR closed the earlier buying and selling day at $252.5.

This represents a 75.6% lower from MSTR’s July 2021 excessive of $1,304. Mixed with Bitcoin’s value volatility, the sharp drop within the firm’s inventory value previously two years pushed many to criticize MicroStrategy’s treasury administration technique and even actively quick it.

On this report, CryptoSlate dives deep into MicroStrategy and its holdings to find out whether or not its formidable guess on Bitcoin makes its inventory at the moment undervalued.

MicroStrategy’s Bitcoin holdings

As of Mar. 1, 2023, MicroStrategy held 132,500 BTC acquired at an combination buy value of $3.992 billion and a median buy value of roughly $30,137 per BTC. Bitcoin’s present market value of $22,300 places MicroStrategy’s BTC holdings at $2.954 billion.

The corporate’s Bitcoins had been acquired by means of 25 totally different purchases, with the most important one made on Feb. 24, 2021. On the time, the corporate bought 19,452 BTC for $1.206 billion when BTC was buying and selling at just below $45,000. The second largest buy was made on Dec. 21, 2020, when it acquired 29,646 BTC for $650 million.

Throughout Bitcoin’s ATH in the beginning of November 2021, the 114,042 BTC MicroStrategy held was price properly over $7.86 billion. Bitcoin’s hunch to $15,500 in early November 2022 valued the corporate’s holdings at simply over $2.05 billion. On the time, the market capitalization of all MSTR inventory reached $1.90 billion.

As CryptoSlate evaluation confirmed, it wasn’t till the tip of February 2023 that MicroStrategy’s market cap received on par with the market worth of its Bitcoin holdings. The discrepancy between the 2 is what prompted many to wonder if MSTR could possibly be undervalued.

Nonetheless, figuring out over or undervaluation requires extra than simply taking a look at MicroStrategy’s market cap.

MicroStrategy’s debt

The corporate has issued $2.4 billion of debt to fund its Bitcoin purchases. As of Dec. 31, 2022, MicroStrategy’s debt consists of the next:

- $650 million of 0.750% convertible senior notes due 2025

- $1.05 billion of 0% convertible senior notes due 2027

- $500 million of 6.125% senior secured notes due 2028

- $205 million below a secured time period mortgage

- $10.9 million of different long-term indebtedness

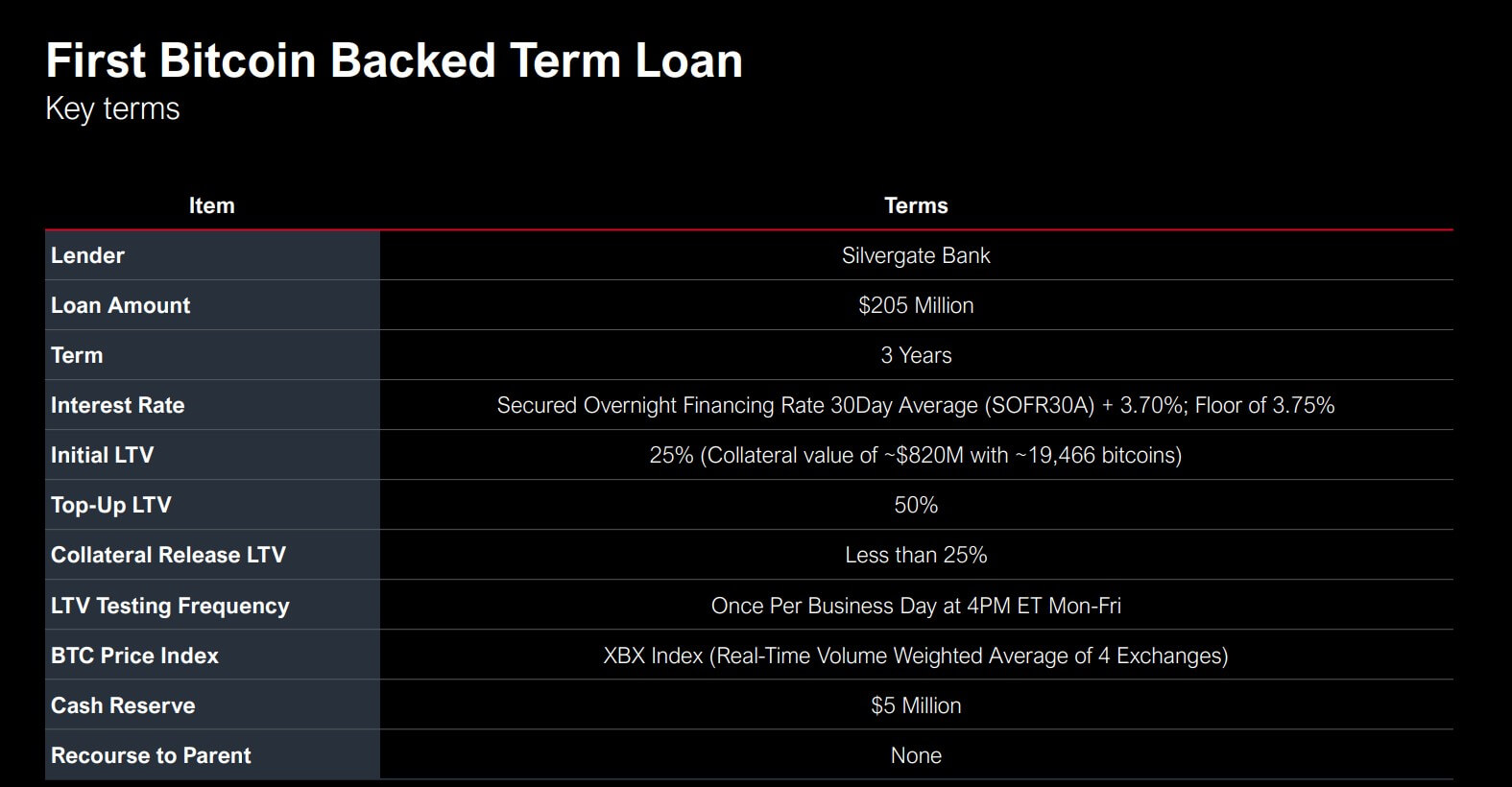

The charges the corporate secured on the 2025 and 2027 convertible notes proved vastly useful, particularly in mild of the just lately rising rates of interest. Nonetheless, the advantages MicroStrategy accrued on the convertible notes are offset by the dangers it took on with its $205 secured time period mortgage from Silvergate financial institution in March 2022.

The mortgage was collateralized with 19,466 BTC, price $820 million on the time, with an LTV ratio of 25%. Till it matures in March 2025, the mortgage should stay collateralized with a most LTV ratio of fifty% — if LTV passes 50%, the corporate will likely be required to prime up its collateral to deliver the ratio again right down to 25% or much less.

Terra’s crash in June 2022 brought about volatility available in the market that required MicroStrategy to deposit a further 10,585 BTC into the collateral. Along with unstable Bitcoin costs, the floating charge Silvergate’s mortgage bears resulted in an annualized rate of interest of seven.19%, placing vital pressure on the corporate.

The latest controversy surrounding Silvergate, coated by CryptoSlate, prompted many to fret about the way forward for MicroStrategy’s mortgage. Nonetheless, the corporate famous that the way forward for the mortgage isn’t depending on Silvergate and that the corporate would continue paying off the mortgage even when the financial institution went below.

Of the 132,500 BTC the corporate holds, solely 87,559 BTC are unencumbered. Apart from the 30,051 BTC used as collateral for the Silvergate secured time period mortgage, MicroStrategy put 14,890 BTC as a part of the collateral for the 2028 senior secured notes. If the collateral for the Silvergate mortgage would should be topped off, the corporate might dip into the 87,559 unencumbered BTC.

Saylor additionally famous that the corporate might put up different collateral if Bitcoin’s value fell under the $3,530 that will set off a margin name on the mortgage.

MSTR vs BTC

One of many greatest stars of the dot com increase, MicroStrategy has seen its inventory undergo intervals of intense volatility in instances of growth.

Following its 1998 IPO, MSTR noticed its value improve by over 1,500%, peaking in February 2000 at over $1,300. After a spectacular value drop that marked the start of the dot com crash, it took the corporate greater than ten years to regain the $120 share value it posted in 1998.

Earlier than its first Bitcoin buy in August 2020, MicroStrategy’s inventory traded at $160. September introduced on a notable rally that pushed its value to a brand new peak of $1,300 in February 2021.

Since then, MSTR posted a notable correlation to Bitcoin’s value actions, with the corporate’s efficiency now tied to the crypto market.

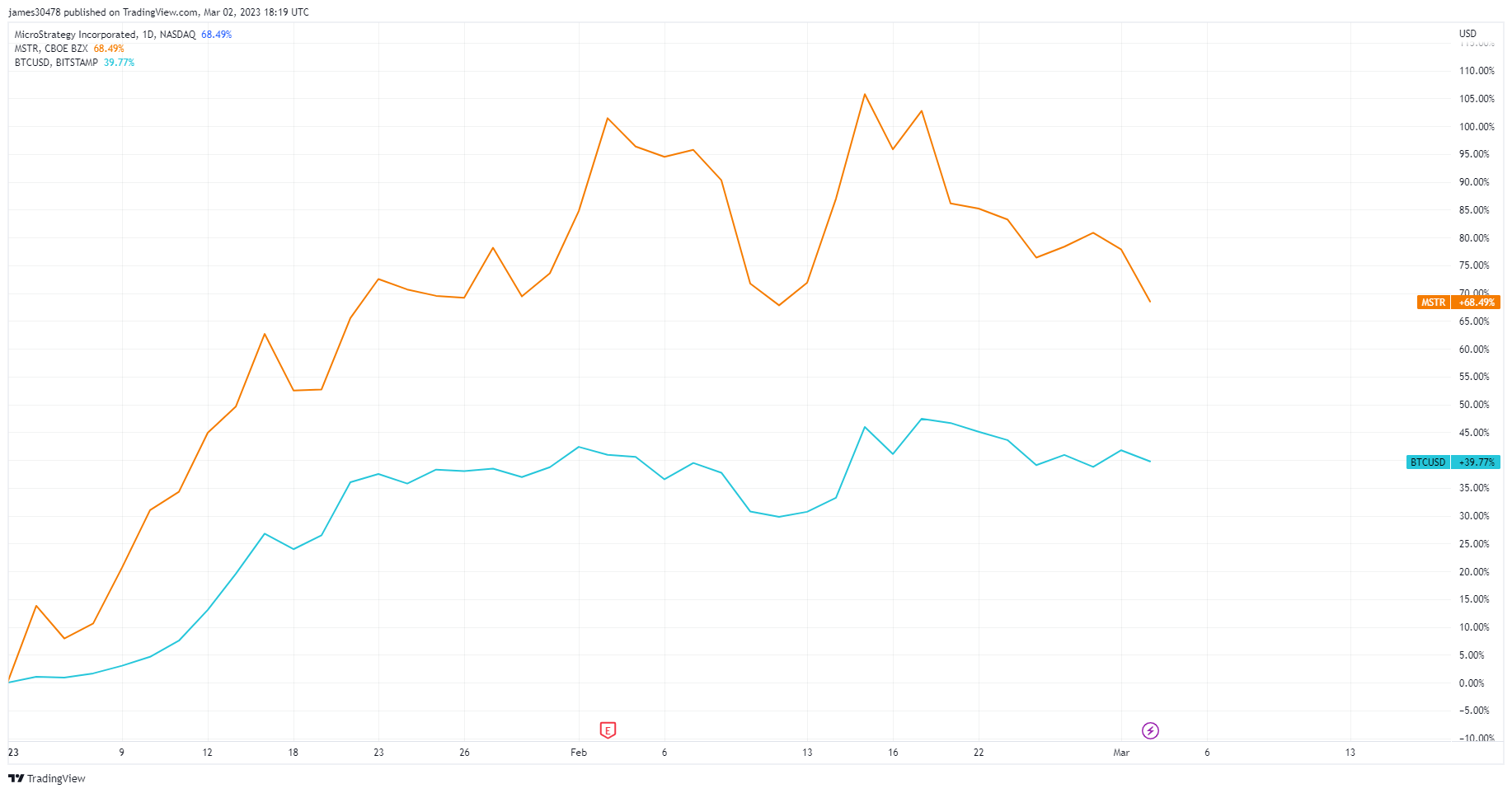

Up over 68% because the starting of the 12 months, MSTR has outperformed BTC, which noticed its value improve by just below 40%.

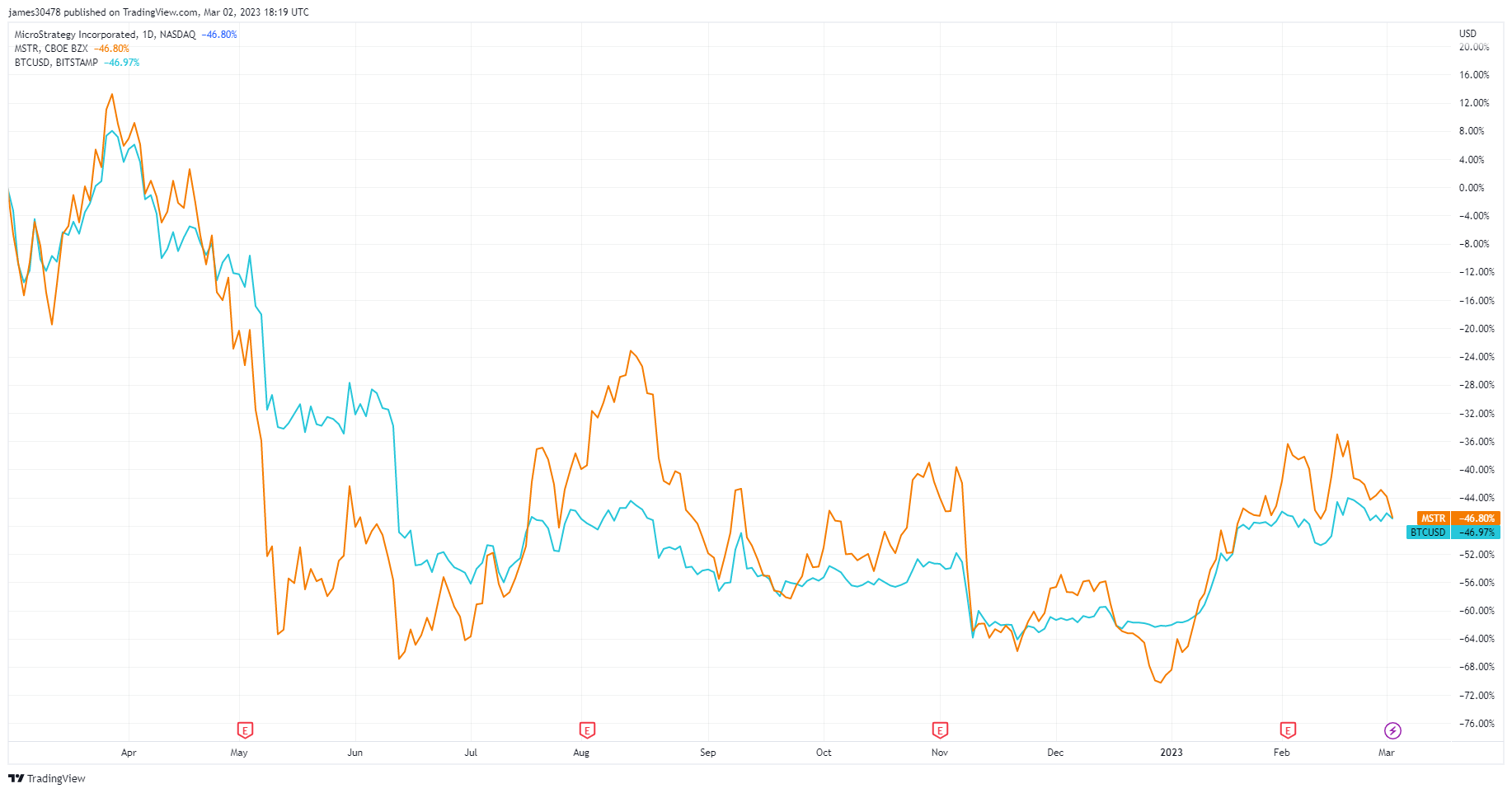

MSTR adopted Bitcoin’s efficiency on a one-year scale as each posted a 46% loss.

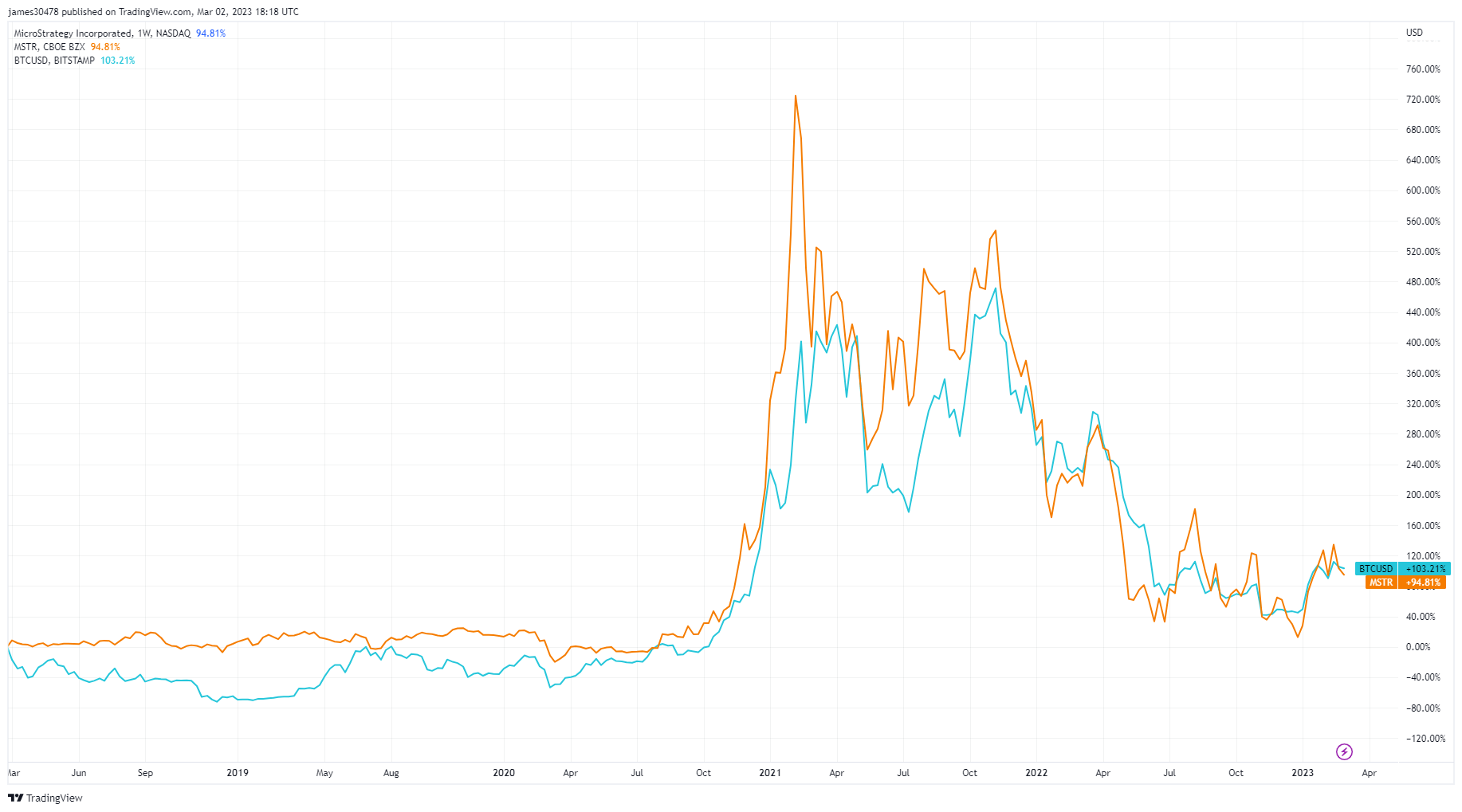

Zooming out to a five-year timeframe reveals a notable correlation in efficiency, with BTC barely outperforming MSTR with a 103% improve.

Nonetheless, MSTR’s market efficiency has usually been overshaddowed by MicroStrategy’s worsening monetary statements. On the finish of the fourth quarter of 2022, the corporate reported an working lack of $249.6 million, up from $89.9 million within the fourth quarter of 2021. This introduced the corporate’s whole working loss for 2022 to $1.46 billion.

The accounting conundrum

With an working lack of $.1.46 billion in 2022, a dangerous mortgage that will require re-collateralization, and a unstable crypto market behind it, MicroStrategy definitely doesn’t look overvalued.

Nonetheless, the corporate’s reported working loss could be obfuscating its profitability. Specifically, the SEC requires firms to report unrealized quarterly losses on their Bitcoin holdings as impairment losses. In accordance with MicroStrategy’s Bitcoin Accounting Remedy, the corporate’s impairment loss provides to its working loss. Which means that a adverse change in Bitcoin’s market value reveals up as a considerable loss on MicroStrategy’s quarterly statements, although the corporate hasn’t offered the asset.

On Dec. 31, 2022, the corporate reported an impairment lack of $2.15 billion on its Bitcoin holdings for the 12 months. It reported an working lack of $1.32 billion earlier than taxes.

Conclusion

Given MSTR’s correlation to Bitcoin’s efficiency, a bull market rally might push the inventory again to its 2021 excessive.

The standard monetary market has traditionally had hassle maintaining with the speedy tempo of development seen within the crypto trade. The type of volatility the crypto market has turn into accustomed to, each constructive and adverse, continues to be a uncommon incidence within the inventory market. In a bull rally much like the one which took Bitcoin to its ATH, MSTR might considerably outperform different tech shares, together with the large-cap FAANG giants.

Nonetheless, whereas MSTR’s development might mimic the expansion seen within the crypto market, it’s extremely unlikely that the corporate will see any vital volatility in its inventory value within the subsequent couple of years. If MicroStrategy continues to service its money owed, will probably be extraordinarily well-positioned to reap the advantages of a crypto-heavy market within the coming decade.

Its longstanding status might make it a go-to proxy for establishments to get publicity to Bitcoin, creating demand that retains shopping for stress excessive.