Analyst Weekly, December 22, 2025

After spending most of the past two years in the penalty box, financials are quietly staging a comeback. Earnings are improving, capital markets are thawing, and valuations are starting to look more like the pre-crisis era than the post-GFC hangover. But selectivity is key: this recovery is uneven, and not everyone gets a trophy.

Earnings: Doing More Than Just Surviving

Financials delivered their second-strongest earnings season in the S&P 500, clocking ~25% year-over-year growth, trailing only Tech. The fundamentals are strong: higher trading revenues, record investment-grade debt issuance, and early signs of life in IPOs and M&A.

Analysts are taking notice. Earnings revisions for both 2025 and 2026 are positive across most Financials sub-industries, with banks and consumer finance leading the pack.

Capital Markets Are Waking Up

2025 has shaped up to be the second-highest year ever for investment-grade issuance, powered by AI-driven capex, refinancing needs, and big corporate balance sheets finally pulling the trigger. M&A volumes are running above 2021 levels, even if some mega-deals are taking their time to close. IPO volumes are tracking near long-term averages after the 2022-2023 freeze.

Valuations

Here’s where it gets interesting. Financials are drifting back toward pre-GFC return-on-equity and price-to-book profiles. That creates room for further multiple expansion, especially as earnings continue to improve and regulatory pressure eases. Compared with other cyclical sectors, Financials still look reasonably priced for the growth they’re delivering.

Policy Is a Tailwind

Macro policy is finally cooperating. Expectations for more accommodative monetary policy in 2026, combined with a lighter regulatory touch, could help offset recent tightening in financial conditions. Lower compliance costs and a friendlier backdrop for lending and capital markets are exactly what the sector needs to extend this recovery.

The Fine Print: It’s a Two-Speed Sector

Not everything is rosy. Private credit remains the biggest risk, with lingering stress after recent high-profile defaults. Consumer rates — credit cards, auto loans, mortgages — are still elevated, offering only marginal relief for households. That keeps pressure on consumer finance and parts of regional banking.

Winners vs. Laggards

Big banks are still the backbone of the trade. Names like JPMorgan and Bank of America continue to hold leadership positions and provide stability. Investment banking and private-credit-exposed names? Still working through issues.

Investment Takeaway: Financials aren’t in a straight-line bull run but they’re no longer just a value trap. With improving earnings, reviving deal activity, and valuations that haven’t fully repriced, the sector looks like a cyclical comeback story: just one that rewards selectivity over blind enthusiasm.

Crypto Markets: 2026 Outlook

As we approach 2026, bitcoin and the broader crypto ecosystem are being shaped by a dual transition: a return of macro liquidity and a structural reconfiguration of the mining and energy landscape driven by artificial intelligence. Price action is currently secondary to positioning, derivatives dynamics, and long-term infrastructure shifts.

Macro Backdrop: Liquidity is Returning

Quantitative tightening is effectively over; markets are transitioning toward monetary easing. Rate cuts by the Federal Reserve are largely priced in. Political incentives in the US point to incremental fiscal and monetary stimulus ahead of mid-term elections. Historically, this environment is supportive for high-beta, liquidity-sensitive assets, including Bitcoin. Short-term price weakness is macro-technical rather than structural, amplified by global rate adjustments (notably Japan) and carry-trade unwinds.

Price Action

BTC is currently consolidating in the $85,000–$90,000 range, reflecting sideways-to- bearish short-term momentum. Expectation: price continues to gravitate toward option-dense levels rather than trending decisively absent a macro catalyst.

Flow Dynamics: Weak Hands vs Patient Capital

- Volume has collapsed, signaling a volatility compression phase.

- Short-term flows show:

- Retail selling small positions under stress.

- Larger players placing deep limit bids, not visible in spot trades.

Conclusion: distribution is retail-led; whales and smart money are waiting,

Institutional Positioning & ETFs

Institutional positioning has quietly stabilised and selling pressure through ETF vehicles has slowed meaningfully. On the corporate side, most large treasury buyers built positions between late 2024 and Q3 2025 at price levels around $80,000–$90,000 and above, leaving current spot prices close to or below recent institutional cost bases. Outside of MicroStrategy, there are few active corporate buyers today, but that absence reflects digestion rather than capitulation. The implication is straightforward: current levels offer a relative entry advantage versus where corporates have already committed capital.

Investment Takeaway: Liquidity conditions are improving, but near-term price action is being driven more by derivatives positioning than by long-term holders. Retail sentiment remains fragile, while institutional positioning is patient and largely intact. Historically, periods marked by low volatility, compressed volume, and narrative discomfort have tended to precede the next major regime shift in Bitcoin’s cycle.

Oil Struggles for Stability: Double Bottom or Just a Brief Pause?

Oil prices closed last week 1.4% lower at $56.50 per barrel. WTI temporarily came very close to the yearly low, which was set in April at $54.83. Toward the end of the week, however, prices rebounded, reflected in the chart by a long lower wick.

Whether this marks the formation of a medium-term double bottom remains uncertain at this stage. Further confirmation would be required, for example, a move back above the $60–$61 area. This zone has been a key battleground since March, alternating between support and resistance.

As long as a sustained breakout above that level fails to materialize, the risk remains that oil prices come under renewed pressure and retest the yearly low. A break below that level would imply a move to the lowest price since January 2021.

Oil price (WTI) weekly chart. Source: eToro

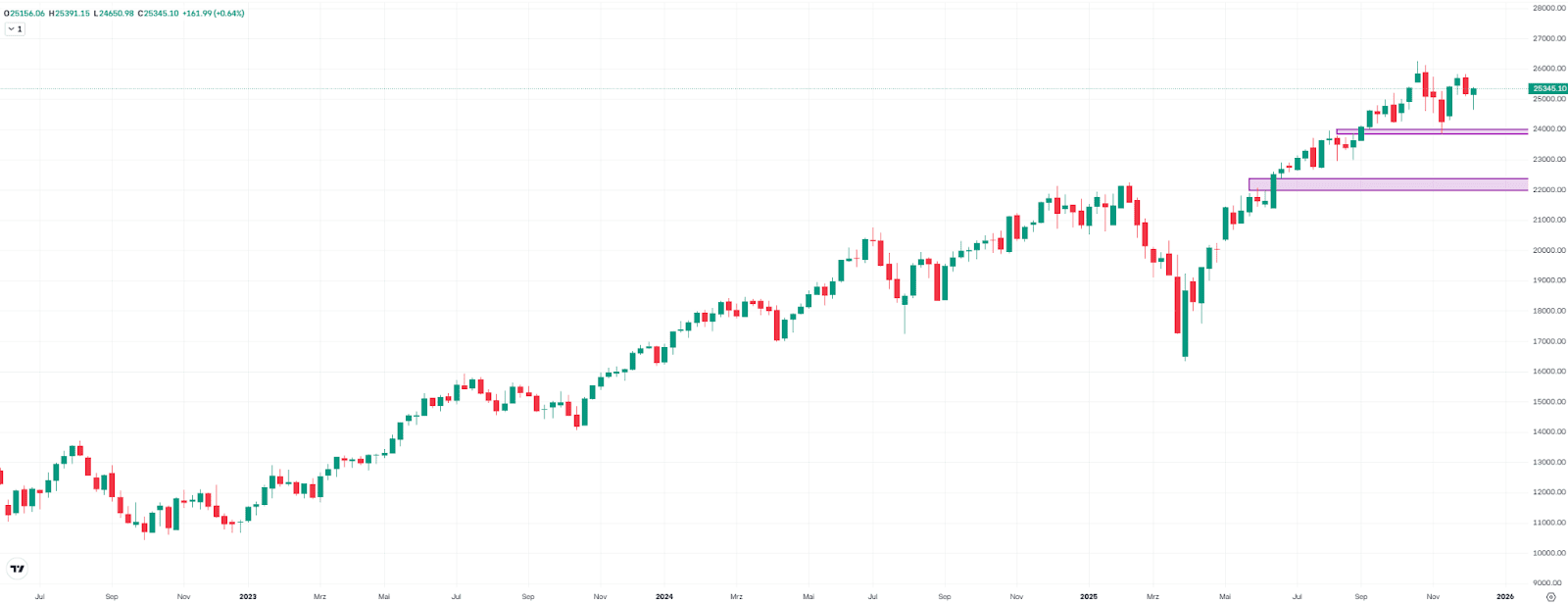

Nasdaq 100 Turns Positive: Is a Push Toward the Record High Next?

Thanks to a strong finish to the trading week, the Nasdaq 100 managed to fully recover its earlier losses and even ended the week up more than 0.6% at 25,345 points. As a result, the gap to the record high from late October has narrowed to less than 4%.

From a technical perspective, a test of the record high appears the most likely scenario given the still-intact uptrend structure. Looking back to December 2024, the setup looks similar. At that time, however, bulls ran out of momentum in the final trading days of the year.

Should the market come under short-term pressure, attention would initially turn to the well-known support zone (fair value gap) between 23,860 and 23,993 points. Below that, the next significant support area lies between 21,980 and 22,375 points. A decline into this second zone would represent a moderate correction.

Nasdaq 100 weekly chart. Source: eToro

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.

? History, Mining, Supply, and Risks")